Pharmacy retail pricing in 2026 has evolved into one of the most complex pricing environments in Latin America. Unlike grocery, pharmacies operate at the intersection of regulated healthcare products, discretionary retail, and data-driven personalization. This creates both constraints and opportunities.

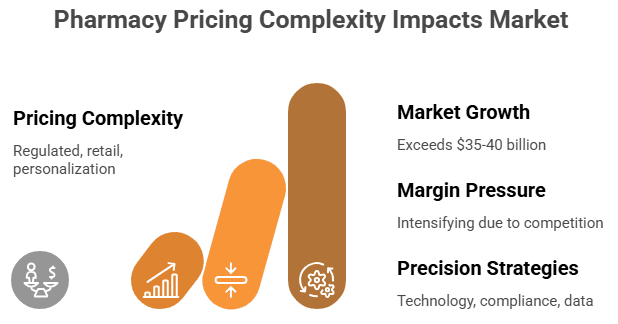

Figure 1: Pharmacy Pricing Complexity Impacts Market in Mexico

In Mexico, the pharmacy sector is projected to exceed $35–40 billion USD in market size by 2027, with steady annual growth of 5–7%, driven by aging populations, chronic disease prevalence, and expanding health access. However, margin pressure is intensifying due to e-commerce competition, regulatory scrutiny, and shifting consumer expectations.

Winning in this environment requires precision pricing strategies by category, supported by technology, compliance guardrails, and data intelligence.

Why Pharmacy Pricing Is More Complex Than Grocery

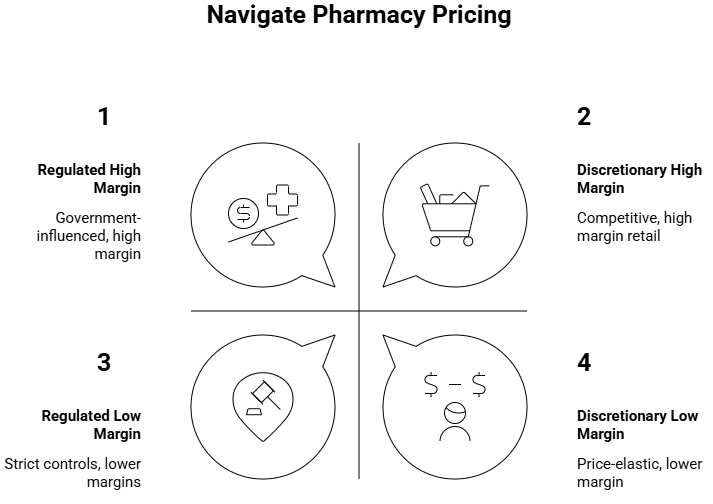

Pharmacy retail combines three fundamentally different pricing logics:

Figure 2: Navigate Pharmacy Pricing

Regulated Products (Prescription & Controlled Substances)

● Prices are influenced by government frameworks and compliance requirements

● Strict controls on substitution, discounting, and promotion

● High compliance risk → pricing errors can lead to sanctions or store closures

In Mexico, regulatory oversight bodies impose strict standards on:

● Drug labeling and authorization

● Price transparency

● Distribution compliance

These constraints reduce flexibility compared to grocery pricing.

OTC & Private Label (High-Margin Opportunity)

Over-the-counter (OTC) and private label products represent the largest margin expansion lever in pharmacy retail.

● Private label margins: 30–60% higher than branded equivalents

● OTC penetration in some chains exceeds 40% of total transactions

● Customers show increasing willingness to switch for price-sensitive categories

Examples of high-performing private label categories:

● Pain relief

● Vitamins and supplements

● Generic personal care

Insight: Leading pharmacy chains are no longer just distributors of brands—they are becoming brand owners.

Health & Beauty (Discretionary Retail Layer)

Pharmacies increasingly overlap with beauty and personal care retail:

● Categories such as skincare, cosmetics, and wellness products deliver gross margins of 40–70%

● Purchase behavior is less regulated and more price-elastic

● Strong exposure to e-commerce price transparency

This creates a dual dynamic:

● Regulated healthcare → rigid pricing

● Beauty & wellness → competitive, dynamic pricing

The Bifurcation of Pharmacy Categories

A critical structural shift in pharmacy retail is the clear split between two economic models:

| | | | | | :-: | :-: | :-: | :-: | | **Category Type** | **Characteristics** | **Margin Profile** | **Role** | | **Essential Health Products** | Prescription drugs, chronic treatments | Low margin (5–15%) | Traffic driver | | **Discretionary Products** | Beauty, wellness, supplements | High margin (30–70%) | Profit driver |

Key insight: Pharmacies must stop treating pricing as uniform. Instead, they should adopt category-specific pricing strategies aligned to role.

E-commerce Disruption: Where Margin Is Under Attack

Online pharmacies and marketplaces are reshaping pricing expectations:

● Price transparency has increased by >80% in discretionary categories

● Online players often undercut physical stores by 10–25% on non-regulated items

● Fast delivery and subscription models reduce switching friction

The impact is asymmetric:

● Essentials: Less affected (due to immediacy and prescriptions)

● Discretionary: Highly exposed to price comparison

Result: Margin compression is concentrated in the very categories that historically funded profitability.

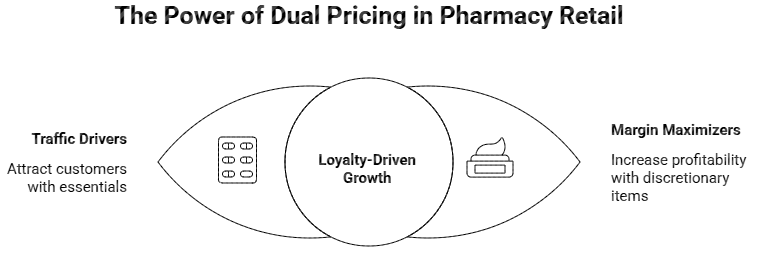

Strategic Response: Traffic vs. Margin Optimization

Leading pharmacy retailers are shifting toward a dual pricing strategy:

Figure 3: The Power of Dual Pricing in Pharmacy Retail

Use Essentials to Drive Traffic

● Maintain competitive or regulated pricing

● Focus on availability, trust, and proximity

● Leverage prescriptions and chronic care programs

Extract Margin from Discretionary & Private Label

● Implement dynamic pricing on OTC and beauty

● Expand private label penetration

● Use bundling and promotions strategically

Loyalty Programs as a Pricing Lever

Pharmacies have a unique advantage: health-linked loyalty data

● Repeat purchase cycles (e.g., monthly medications)

● Personalized offers based on health needs

● Cross-selling from prescriptions to OTC and wellness

Retailers leveraging loyalty effectively see:

● 15–25% higher basket sizes

● 2–3x higher retention rates

Case Insight: Integrated Pricing Across Formats

Large retail groups operating both pharmacies and convenience formats are uniquely positioned.

Key advantages:

● Shared supply chain and procurement leverage

● Cross-format pricing intelligence

● Ability to position stores differently by location

Example strategy patterns observed:

● Convenience stores drive impulse and accessibility

● Pharmacies drive trust and health-related traffic

● Pricing alignment ensures no internal cannibalization

This multi-format approach allows:

● Better price architecture across channels

● Improved margin mix optimization

Regulatory Considerations in Mexico

Pricing strategies must operate within strict regulatory frameworks:

Key Compliance Areas:

● Authorization of pharmaceutical products

● Transparency in pricing and labeling

● Restrictions on promotion of certain drug categories

Regulatory bodies enforce:

● Product traceability

● Accurate pricing display

● Controlled discounting practices

Implication: Pricing systems must include compliance guardrails, not just optimization logic.

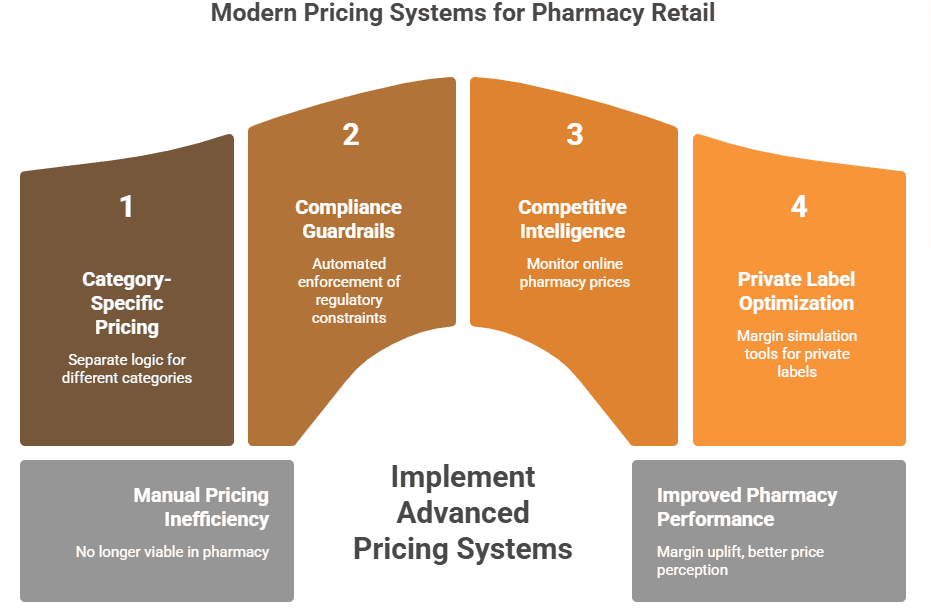

Technology as the Enabler

Manual pricing is no longer viable in pharmacy retail.

Modern Pricing Capabilities Required:

Figure 4: Modern Pricing Systems for Pharmacy Retail

Category-Specific Pricing Rules

● Separate logic for prescription, OTC, and beauty

● Elasticity-based pricing for discretionary categories

Compliance Guardrails

● Automated enforcement of regulatory constraints

● Real-time alerts for pricing violations

Competitive Intelligence

● Monitoring online pharmacy and marketplace prices

● Identifying undercutting risks in key SKUs

Private Label Optimization

● Margin simulation tools

● Price positioning vs. branded alternatives

Retailers implementing advanced pricing systems report:

● 2–5% margin uplift

● 10–15% improvement in price perception

● Faster response to competitive changes

8. Why Pharmacy Retail Remains a Strong Vertical

Despite complexity, pharmacy retail remains highly resilient:

● Healthcare demand is non-cyclical

● Aging populations increase long-term demand

● Chronic conditions drive repeat purchases

However, success depends on digital maturity:

● Data-driven pricing

● Integrated omnichannel strategy

● Category-level optimization

Retailers that fail to modernize risk:

● Margin erosion in discretionary categories

● Loss of price competitiveness online

● Regulatory exposure

Conclusion

Pharmacy pricing in 2026 is no longer about setting prices—it is about orchestrating a multi-layered system balancing regulation, competition, and profitability.

The winning formula is clear:

● Protect traffic with essential products

● Drive margin through discretionary and private label

● Leverage loyalty data for personalization

● Embed compliance into pricing systems

● Adopt category-specific, technology-driven pricing

Pharmacy retailers that embrace this complexity will not only survive—but lead.

Sources & Market References

● Industry pharmaceutical market growth estimates (IQVIA, OECD health data)

● Latin America retail pharmacy trends (Statista, Euromonitor)

● Private label margin benchmarks (McKinsey retail reports)

● E-commerce pricing impact studies (Bain & Company, Deloitte retail insights)

● Regulatory frameworks (Mexican health regulatory authority publications)

Ready to Go Deeper?

Request our Pharmacy Retail Pricing Guide to explore:

● Category-level pricing frameworks

● Private label optimization models

● Compliance-ready pricing systems

● Benchmarks across leading pharmacy retailers

Visit:www.rapidpricer.com

*"*AI-Generated Content Disclaimer

*This content was generated in part with the assistance of artificial intelligence tools. While efforts have been made to review, edit, and ensure the accuracy, completeness, and reliability of the content, it may still contain errors or omissions. It should not be considered professional advice, and users should independently verify any information before making decisions based on it. The publisher/author assumes no responsibility or liability for any consequences resulting from reliance on this content."*

Read More On

● The E-commerce Pricing Arms Race: Why Mexican Retailers Need Real-Time Intelligence, Not Just Software

● Hyperlocal Pricing for 20,000 Micro-Locations: How Large Convenience Retailers Can Unlock Revenue Growth

● The Grocery Pricing Trilemma in Latin America: Fresh Products, Inflation, and Competitive Pressure

● Private Label vs. National Brands: The Pricing Tightrope in Hard Discount & Pharmacy Retail

● The Hard Discount Pricing Paradox: Pricing 500+ New Stores

About RapidPricer

RapidPricer helps automate pricing and promotions for retailers. The company has capabilities in retail pricing, artificial intelligence, and deep learning to compute merchandising actions for real-time execution in a retail environment.

Contact info:

Website:

LinkedIn:

Email: info@rapidpricer.nl